3 Top Performing Multi Asset Allocation Funds 2026 – Must Watch

A Multi Asset Allocation Fund is designed to invest across at least three asset classes (commonly equity, debt, and gold/commodities), with SEBI rules widely summarized as requiring a minimum 10% allocation to each asset class. These funds aim to reduce single-asset dependence and simplify rebalancing for long-term investors. For 2026, a practical way to judge the best multi asset allocation funds is to compare not only returns (3Y/5Y) but also risk ratios like standard deviation and Sharpe, using direct-plan growth options for a fair comparison.

Disclaimer: Educational content only. Mutual fund investments are subject to market risks. Please read all scheme-related documents and consider a SEBI-registered advisor for personalized guidance.

Multi Asset Allocation Fund: What It Is and Why It Fits 2026 Portfolios

Definition (featured snippet, ~80–100 words):

A Multi Asset Allocation Fund is a hybrid mutual fund that invests across at least three asset classes—typically equity (growth), debt (stability), and gold/commodities (hedge). Industry explainers and AMC guidance commonly note SEBI’s requirement that multi-asset allocation funds maintain a minimum 10% allocation to each of the chosen asset classes. The core idea is simple: when one asset struggles, another may cushion the fall—helping investors stay invested through cycles.

Why investors are watching this category in 2026

Volatility is normal: Equity can swing; debt responds to rate cycles; gold can act as a hedge.

Rebalancing advantage: Multi-asset funds can adjust allocations within the scheme (based on mandate).

Simple “one-ticket” diversification: Good for investors who don’t want to manage multiple funds.

AMFI’s investor education pages also describe multi-asset funds as offering broad exposure across asset classes.

Best Multi Asset Allocation Funds: How “Top Performing” Should Be Measured

If you want a credible “top performing” list, don’t look at returns alone. Use a two-lens evaluation:

Lens A — Returns (what you earned)

1Y/3Y/5Y CAGR (avoid only short-term rankings)

SIP returns (if you invest monthly)

Lens B — Risk-adjusted performance (how bumpy it was)

Standard deviation: higher = more volatility

Sharpe ratio: higher = better risk-adjusted returns (in general)

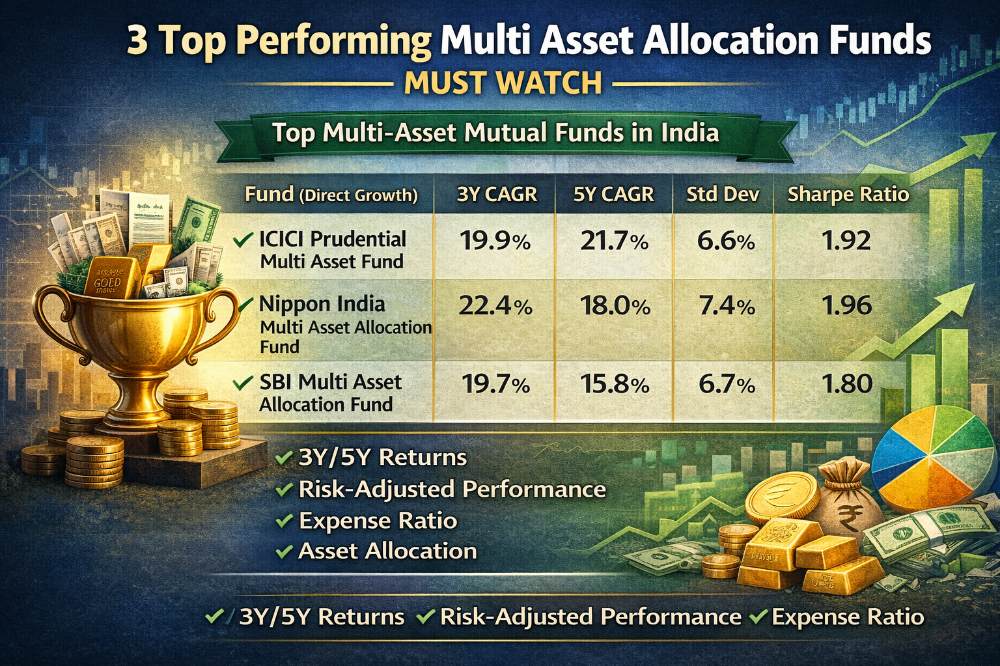

A recent comparison of three prominent multi-asset funds reported 3Y/5Y CAGR alongside standard deviation and Sharpe ratio, explicitly using Direct Plan + Growth for apples-to-apples evaluation.

Direct plan vs regular plan (why it matters)

Direct plans usually have lower costs than regular plans—over years, cost differences can meaningfully impact compounding. When comparing funds online, confirm you’re comparing the same plan and option.

3 Top Performing Multi Asset Allocation Funds 2026: Quick Snapshot Table (Must Watch)

Based on a January 2026 comparison using fund factsheets (Direct Plan, Growth), these are commonly highlighted as the “top 3” to watch:

Source noted: Fund factsheets (as summarized in Jan 2026).

How to read this quickly:

If you prioritize higher 5Y CAGR, ICICI Prudential (in this comparison) stands out.

If you prioritize higher 3Y CAGR, Nippon leads here.

If you want lower volatility, ICICI/SBI show lower standard deviation in this snapshot.

Reality check: Rankings can change with market cycles. Use this as a shortlist, then validate with the latest factsheets and your risk profile.

Fund #1 Deep Dive: ICICI Prudential Multi Asset Fund (Performance + Risk)

What it is (in plain English)

ICICI Prudential Multi Asset Fund is positioned as a multi-asset approach combining growth assets (equity) with stabilizers (debt) and diversifiers/hedges (often gold/commodities). In the Jan 2026 comparison, it showed strong 5-year CAGR and a relatively lower standard deviation among the three.

Who it may suit

Investors aiming for long-term wealth creation but who dislike extreme drawdowns

Those who want a core hybrid holding rather than a tactical bet

SIP investors who want smoother ride vs pure equity

What to verify in the factsheet before investing

Use this checklist:

Current asset mix (equity/debt/commodity %)

How often allocations change (rebalancing behavior)

Credit quality of debt portion (avoid unpleasant surprises)

Exposure concentration (top holdings weight, sector tilts)

Fund #2 Deep Dive: Nippon India Multi Asset Allocation Fund (Performance + Risk)

Why it’s on the 2026 “must watch” list

In the same snapshot comparison, Nippon India Multi Asset Allocation Fund showed the highest 3-year CAGR and the highest Sharpe ratio among the three listed funds.

Other public trackers also show it appearing near the top across multiple time windows (depending on filter/period).

When it can shine

When equity trends favor the fund’s style allocations

When diversification sleeve (gold/commodity) adds protection in risk-off phases

When the fund’s rebalancing captures mean reversion

Common investor mistakes

Buying after a great short-term run without checking current allocation

Ignoring volatility: higher returns often come with higher swings (Std Dev is higher in the snapshot)

Treating it like a guaranteed “balanced” product without reading mandate and asset behavior

Fund #3 Deep Dive: SBI Multi Asset Allocation Fund (Performance + Risk)

Why it’s relevant for 2026 investors

In the same comparison, SBI Multi Asset Allocation Fund showed competitive 3-year CAGR with volatility similar to ICICI (Std Dev close), but lower 5-year CAGR than the other two in that snapshot.

Ideal use cases

Investors who want a multi-asset core with a disciplined structure

Those who prefer strong brand/AMC processes and straightforward allocation style

People building a hybrid base and adding equity funds separately

How to compare fairly

Compare:

Direct plan growth vs direct plan growth

3Y/5Y with category average

Sharpe ratio and volatility—not only returns

Best Multi-Asset Mutual Funds in India 2026: Selection Checklist (10-point)

Use this checklist to shortlist the best multi asset allocation funds for your needs:

Mandate compliance: at least 3 assets, minimum 10% each (confirm)

Return consistency: check 3Y + 5Y, not only 1Y

Risk ratios: Std Dev + Sharpe in the same plan/option

Asset allocation discipline: frequent extreme shifts can surprise you

Debt quality: credit profile matters in stress markets

Gold/commodity role: hedge or return driver? Know what you’re buying

Costs: expense ratio differences compound over time

Portfolio overlap: avoid accidental concentration via multiple similar funds

AUM and liquidity: very small funds can behave differently than large funds

Your behavior fit: can you stay invested during a 15–25% drawdown?

Multi Asset Allocation Fund Strategy: Core–Satellite Portfolio Examples

A practical way to use multi-asset funds is Core–Satellite:

Conservative (stability-first)

60–80%: Debt/balanced instruments

20–40%: Multi asset allocation fund as a diversified growth sleeve

Balanced (most common)

50–70%: Multi asset allocation fund (core)

30–50%: Equity index/flexicap for additional growth

Aggressive (growth-first)

30–50%: Multi asset allocation fund (shock absorber)

50–70%: Equity funds (index + style diversification)

Rebalancing rule (simple):

Review every 6–12 months

Rebalance if an allocation drifts by 5–10% from target

This helps you avoid the classic mistake: becoming unintentionally concentrated right before a correction.

Taxes, Costs, and Practical Buying Tips (SIP vs Lump Sum)

SIP vs lump sum (what to choose)

SIP: best for most investors; reduces timing risk and builds discipline

Lump sum: works when valuations are attractive and you have high risk tolerance

Cost factors that matter

Expense ratio: lower costs can improve long-term compounding

Exit load: check holding period requirements

Turnover/transaction impact: frequent churn can affect efficiency

Practical execution steps (numbered for snippets)

Choose Direct Plan + Growth for comparison clarity

Decide time horizon (minimum 3–5 years; ideally longer)

Pick SIP date and stick to it

Review annually; avoid reacting to short-term noise

Validate fund allocations with factsheets

FAQs + 30-Day Action Plan: Choose the Best Multi Asset Allocation Funds Confidently

30-day action plan

Week 1: shortlist 5 funds; filter by 5Y + risk ratios

Week 2: read factsheets (allocation, debt quality, top holdings)

Week 3: pick 1–2 funds; set SIP; define rebalancing rule

Week 4: set a review calendar; track KPIs monthly

FAQs

1) What is a Multi Asset Allocation Fund?

A Multi Asset Allocation Fund invests across at least three asset classes—commonly equity, debt, and gold/commodities. The structure aims to reduce dependence on one asset type and can help manage volatility through diversification and internal rebalancing. Many AMC explainers summarize SEBI’s requirement as maintaining at least 10% allocation to each asset class used.

2) Which are the best multi asset allocation funds in India for 2026?

A widely shared January 2026 comparison shortlist includes ICICI Prudential Multi Asset Fund, Nippon India Multi Asset Allocation Fund, and SBI Multi Asset Allocation Fund, evaluated on 3Y/5Y CAGR and risk metrics (Std Dev, Sharpe) using Direct Plan Growth. Always verify latest factsheets before deciding.

3) Are multi-asset funds safer than equity funds?

They can be less volatile than pure equity because debt and gold/commodities may cushion downturns, but they still carry market risk. “Safer” depends on allocation mix and market regime. Evaluate standard deviation and Sharpe ratio rather than relying on labels.

4) Should I choose multi-asset funds for SIP?

Often yes—multi-asset funds can be a good SIP vehicle because they combine diversification with professional allocation. SIP also reduces timing risk compared to lump sum investing.

5) What time horizon is best for multi-asset funds?

Aim for at least 3–5 years, preferably longer. Short-term performance can swing based on equity, rate cycles, and gold movements.

6) How do I compare multi-asset funds properly?

Compare Direct Plan Growth to Direct Plan Growth. Look at 3Y/5Y CAGR, standard deviation, and Sharpe ratio. Then check factsheets for asset allocation stability, debt quality, and concentration.

7) What’s the biggest mistake investors make with “top performing” lists?

Chasing last year’s winners without checking risk, current allocation, or whether the fund’s style matches their risk tolerance. Use performance lists to shortlist—not to decide.

If you want a clean, low-regret approach in 2026: shortlist 3–5 multi-asset funds, compare Direct Plan Growth returns and risk ratios, then start a SIP and review annually. Use the “Top 3 must watch” table above as a starting point—but validate with the latest factsheets before committing.

Powered by Froala Editor

You May Also Like

प्रतिभाओं का सम्मान: बी.एन. पाल प्राथमिक विद्यालय में आफरीन ने मारी बाजी

Hire CakePHP Developers from India

बस्ती: शांति भंग की आशंका में तीन युवकों का चालान

Basti: बलात्कार के वांछित अभियुक्त को कलवारी पुलिस ने किया गिरफ्तार

New Sainik School Opened: 100 नए सैनिक स्कूलों पर फिर जोर: रक्षा मंत्री राजनाथ सिंह ने ट्वीट कर दी जानकारी