HDFC Bank Ranks Third in Large Defaulter Exposure Among Private Lenders

Content Summary

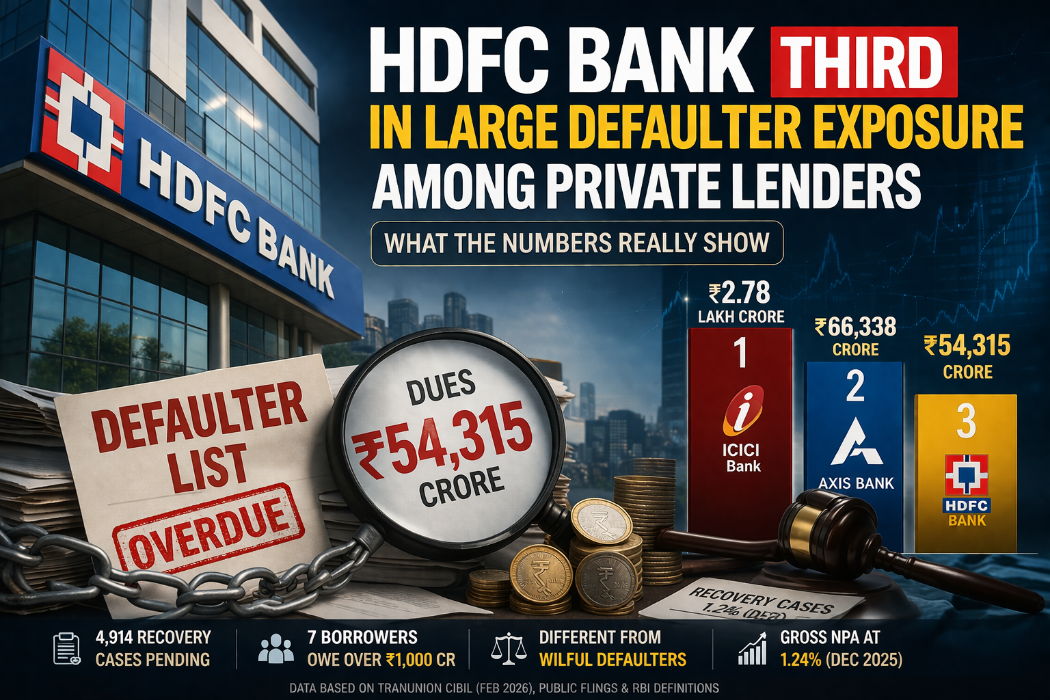

A report citing TransUnion CIBIL data up to February 2026 says HDFC Bank has ₹54,315 crore in “large defaulter” dues and ranks third among major private lenders, behind ICICI Bank (₹2.78 lakh crore) and Axis Bank (₹66,338 crore).

The report says HDFC Bank has 4,914 pending recovery cases and seven borrowers with dues above ₹1,000 crore.

The same report describes “large defaulters” as borrowers with dues above ₹1 crore where banks have filed civil suits, which is broader than the stricter regulatory category of wilful defaulters.

Public bank-wise wilful-default data for 30 September 2025 showed HDFC Bank at ₹640.46 crore, far below its “large defaulter” exposure, underscoring that the two lists measure different kinds of credit stress.

HDFC Bank’s latest reported asset quality remained comparatively stable, with gross NPAs at 1.33% of gross advances as of March 31, 2025, improving to 1.24% by December 31, 2025.

HDFC Bank has emerged as the third-largest private-sector lender by “large defaulter” exposure, according to a new report that cites TransUnion CIBIL data up to February 2026. The report puts HDFC Bank’s dues from large defaulters at ₹54,315 crore, behind ICICI Bank’s ₹2.78 lakh crore and Axis Bank’s ₹66,338 crore.

The same report says HDFC Bank has 4,914 pending recovery cases and that only seven borrowers on its books have dues of more than ₹1,000 crore. Among the biggest named exposures were Feedback Energy Distribution and Feedback Infra at ₹1,876 crore, Sree Rengaraj Ispat Industries at ₹1,764 crore, Riverbank Developers at ₹1,572 crore, and Karvy Stock Broking at ₹1,558 crore.

Crucially, the report is not using the same definition as the RBI’s better-known wilful defaulter framework. It describes “large defaulters” as borrowers with dues above ₹1 crore where banks are pursuing civil recovery suits. RBI’s 2024 directions, by contrast, treat wilful defaulters and large defaulters as separate regulatory concepts, with wilful default requiring findings such as deliberate non-payment, diversion, or siphoning of funds.

That distinction matters because a recovery list can capture a broader universe of stressed accounts than a wilful-default list.

Public bank-wise wilful-default data available for 30 September 2025 showed HDFC Bank at ₹640.46 crore, compared with ICICI Bank at ₹5,620.83 crore, Axis Bank at ₹2,487.60 crore, and Yes Bank at ₹1,565.52 crore. On that narrower list, HDFC Bank was much lower down the ranking. In other words, the new report does not show HDFC Bank as the third-largest private bank by wilful defaulters; it shows the bank as third by one specific large-default recovery measure.

The bank’s broader asset-quality disclosures also paint a more measured picture. HDFC Bank said its gross non-performing assets were 1.33% of gross advances as of March 31, 2025. By December 31, 2025, that ratio had improved to 1.24%, according to its quarterly investor presentation. Those figures suggest the lender’s overall headline asset quality remains relatively contained, even as some older large-ticket exposures continue through recovery channels.

The episode highlights a recurring problem in Indian banking coverage: “defaulters,” “large defaulters,” “wilful defaulters,” and “NPAs” are often used interchangeably when they are not the same. HDFC Bank is India’s largest private lender by assets, so any list tied to unresolved credit stress draws attention. But without the right definitions, a ranking can overstate — or understate — what the data actually mean.

For readers and investors, the takeaway is straightforward: HDFC Bank does appear high on one recent large-defaulter exposure list, but that is not the same as saying it has the third-highest wilful-defaulter burden among private banks. The label attached to the data changes the story.

Powered by Froala Editor

You May Also Like

वायरल वीडियो से बंगाल में सियासी तूफान: हुमायूं कबीर पर BJP से ₹1000 करोड़ की कथित डील का आरोप, PMO और डिप्टी सीएम पद का भी जिक्र

पूर्व इजराइली आर्मी चीफ हरज़ी हलेवी का फोन हैक? फैमिली फोटो, वीडियो और कथित सीक्रेट मीटिंग्स की तस्वीरें लीक

धार हत्याकांड का खुलासा: पत्नी-प्रेमी पर सुपारी देकर मिर्ची कारोबारी की हत्या कराने का आरोप

इंदिरापुरम हाईराइज मौत केस: 16वीं मंजिल से गिरने से 18 वर्षीय लड़की की संदिग्ध मौत, दुष्कर्म-हत्या की आशंका

सूरत में बिना दूध के 1400 किलो पनीर पकड़ा गया: दूध नहीं, पाम ऑयल और एसिड के इस्तेमाल का आरोप